When shopping for a QLAC, there are options to be aware of. These include the company and legal limit that is calculated to purchase a QLAC. But they should also include a review of the annuity carrier through which you are purchasing your Qualifying Longevity Annuity Contract or QLAC. This is because you will want the carrier to be strong and stable from a financial standpoint – and to know that the insurance carrier will continue to pay your income payments on a regular basis.

New York Life’s Company History

The company was founded in 1845 in New York City at 58 Wall Street. New York Life Insurance Company is the largest mutual life insurance company in the United States. A Mutual Life Insurance company is owned entirely by its life and annuity policyholders. Profits are redistributed back to policyholders in the form of dividends.

The main products that are offered by New York Life Insurance Company are life insurance and retirement annuities. The products are offered through licensed “in-house” captive financial advisors throughout the United States, as well as through a limited number of New York Life Insurance Company’s brokerage distribution partners.

New York Life Insurance Company’s Ratings

New York Life Insurance Company has been in the insurance industry for many years, the ratings that the company currently holds are outstanding related to their financial strength and stability. QLAC is usually issued by New York Life’s division called New York Life Insurance & Annuity Company out of Delaware. See the following ratings:

- A++ (Superior) from A.M. Best.

- AA+ from Standard & Poor’s.

- 100 (out of 100) Comdex Rating

New York Life QLAC offering details.

New York Life’s QLAC is called Guaranteed Future Income Annuity II which is a flexible premium deferred income annuity that provides a stream of income payments guaranteed for the life, or lives, of the annuitant(s), beginning on a date chosen by the policy owner.

- Issue Age: QLAC is 31yrs old to 80 yrs old

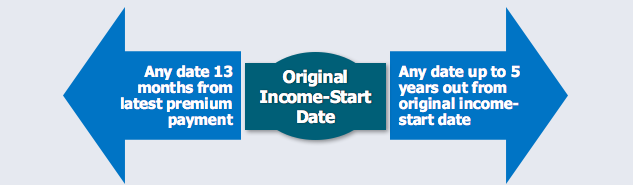

- Income start date: Selected at time of purchase. Flexible income start date feature allows the owner to after the latest premium payment or defer income payments up to five additional years from the original income start date selected.

- Income Modes: Annually, Semi-annually, Quarterly, or Monthly

- Payment Options: Life with Cash Refund. This option guarantees that, if the annuitant (or both annuitants for a Joint Life policy) dies before the income payments received equal the premium paid, the beneficiary(ies) will receive a lump sum equaling the premium less all income payments received.

- Life Only. This option does NOT guarantee a return of deposit at death. Income continues for the life of the annuitant, usually at a higher initial income rate than other income options.

- Optional Features: Annual income increases, COLA. Allows most policy owners to increase income payments each year by 1% to 3%, depending on the percentage chosen at time of deposit.

QLAC Defined

The IRS and Treasury Department have released final regulations on the treatment of Qualifying Longevity Annuity Contracts, or QLACs, under the required minimum distribution (RMD) rules of Internal Revenue Code section 401(a)(9). The final regulations provide an exception to the RMD rules, allowing IRA owners to use a portion of his or her account to purchase a deferred income annuity (DIA), in which annuity payments commence at a specified age, no later than 85, while still satisfying the RMD requirements. Deposits are limited to the lesser of $125,000 or 25% of the owner’s IRA values as of 12/31 of the previous year. The value of the QLAC will be excluded from RMD calculations. The dollar threshold may be increased in future years to reflect changes in the cost of living in $10,000 blocks. Income payment types can be Single Life or Joint Life ( Same Sex Partner or Spouse), and Life with Cash Refund of Deposit. No cash value beyond the initial deposit may present at the time of death of annuitant.

How to use this annuity in retirement planning?

Have your constant lifetime income cover your basic expenses in retirement. This would include any Social Security, Pensions, and annuity income like New York Life’s QLAC called Guarantee Future Income Annuity series. Think of a QLAC as a base line for retirement income along with your social security payments. Having this guaranteed income will allow your other investments to potentially take more risk in turn gaining more return for you.

Studies have shown that converting a small portion, less than 50%, of your retirement funds to an income annuity will increase your retirement portfolio income success rate over a 20-year plus time frame. By eliminating some of your stock market risk with a purchase of Guaranteed Future Income Annuity will produce lifetime income in retirement that cannot be outlived.